Today, financial education starts increasingly early. Many online banks and neobanks now offer debit cards specifically designed for minors, from age 6.

These cards allow teenagers to begin managing their allowance, their first purchases, or their vacation budget, while providing a secure framework for parents.

But then, how are these cards different from a traditional bank card? In this article, we present our top 4 best debit cards for teenagers in 2026, explaining their specifics, their advantages, and who they are really for.

What is a bank card for adolescents?

A bank card designed for teenagers is above all a debit card, never a credit card. Specifically, the money spent corresponds only to the available balance on the associated account, which excludes any risk of overdraft. These cards, accessible from 6, 8, or 10 years old depending on the provider, allow young people to pay for everyday purchases or withdraw money in a secure framework. Parents stay in control thanks to an app that lets them set limits, top up the account, and monitor expenses. It’s a simple and reassuring tool to introduce your child to money management.

Top 4 best minor cards in 2026

Giving your child a bank card is no longer reserved for high school students or college students. Traditional banks such as BNP Paribas, Société Générale, or Crédit Agricole have long offered accounts for minors, with an appropriate card and limited limits. But the landscape has changed a lot, as online banks, neobanks, and fintechs now offer a new generation of debit cards designed to fit young people’s habits. Intuitive mobile apps, real-time notifications, the ability to block the card with one click, etc. Uses are much more modern.

After reviewing various offers available in 2026, four cards stood out to us, whether for their simplicity, practicality, or the positive reception from families: Pixpay, Banxup, BoursoBank and Revolut Kids & Teens.

What is the best bank card for a minor? Our 2026 comparison

How Café de la Bourse made this selection of the best bank cards for teenagers?

The market for teenage bank cards has greatly expanded in recent years. To help parents navigate clearly, we have selected four offers that seem the best to us in 2026. To establish this ranking, several criteria were considered:

- Minimum age of access: some bank cards are available from age 6, others from age 10 or 12

- Pricing: monthly or annual cost, possible free for customers of certain banks

- Payment features: withdrawals, online payments, usage abroad, integration with mobile payments

- Parental control: ability to block the bank card, set limits, or receive real-time notifications

- Educational tools: playful app, budget tracking, missions to learn how to manage money

- Usability and personalization: clarity of the app, card design, services tailored to young users

Based on these criteria we selected Pixpay, Banxup, BoursoBank and Revolut Kids & Teens, four solutions that stand out for their seriousness and adaptability to family needs.

Comparison table of the best bank cards for teenagers in 2026

| Bank card | Minimum age | Pricing | Payment features | Parental control | Educational tools | Usability & personalization |

|---|---|---|---|---|---|---|

| Pixpay | From 8 years old | €3.99/month | Withdrawals, online and abroad payments, compatible with Apple Pay/Google Pay | Instant lock, adjustable limits, real-time notifications | Educational app, missions to learn how to manage your budget | Clear app, modern card, little personalization |

| Banxup | From 10 years old | Free (with a parent account at Société Générale) | Online and in-store payments, withdrawals in France and abroad, instant transfers between friends, Apple Pay and Google Pay compatibility for mobile payments | Real-time expense tracking, setting of payment and withdrawal limits, ability to block/unblock the card at any time, management of permitted payment types | Clear view of expenses, pocket money tracking, transaction history to help the teen understand spending habits | Intuitive and easy-to-use app, real-time notifications, customizable interface with settings tailored to parents and teens |

| Revolut Kids & Teens | From 6 years old | Free (with a Revolut parent account) | Online and in-store payments, limited withdrawals, international payments | Instant notifications, management from the parent app | Basic expense tracking, learning of simple money management | Smooth interface, junior app, card with a simple design |

| BoursoBank 12-17 offer | From 12 years old | Free | Online and in-store payments, withdrawals, international payments | Complete parental monitoring and management of limits | Expense categorization to track your budget | Personalization of notifications |

BoursoBank 12-17 offer: the teens’ bank account

The BoursoBank 12-17 offer isn’t limited to a simple bank card, as it is a full bank account, accessible from age 12 up to 17, reserved for the bank’s online clients’ children. Totally free, the 12-17 offer includes a Visa card with mandatory authorization, initially available virtually and compatible with Apple Pay and Google Pay. After activating the account, you can receive a physical card on request.

The 12-17 BoursoBank offer can be used in France and abroad, with the ability to make payments with a default limit of €200 over 30 days (which can be increased to €5,000) and withdrawals up to €100 over 7 days (which can be increased to €500).

Designed as a tool to learn financial autonomy, the 12-17 BoursoBank offer comes with a dedicated app that allows the teenager to track their balance in real time, customize alerts, and visualize their expenses with pictogram-based categorization. They can also request money from their parents, who receive a notification and can approve the transfer instantly. A savings account (Livret A jeune) associated helps instill good saving habits from a young age.

The 12-17 BoursoBank offer also includes features designed for teens, such as money transfers via SMS, handy for reimbursing a movie ticket or a coffee with friends, even if the friends are not BoursoBank clients. The app also includes a section called The Corner, which houses partner offers and discounts, as well as a referral program that lets you earn a bonus credited directly to the account by inviting friends to join the 12-17 BoursoBank offer.

BoursoBank 12-17 card

Pixpay: the card connected to an educational app

Pixpay is one of the most well-known cards when it comes to teenage banking solutions. Available from age 8, it relies on a Visa card with mandatory authorization, but designed to operate only on debit, with no overdraft possible. The subscription is €3.99 per month, a reasonable price for this type of service. In use, the teen can pay in-store, online, or even abroad, which makes it a truly practical daily tool.

But where Pixpay stands out is its app, because parents can track every expense, set limits, or block the card in seconds, while young people discover tools to learn how to manage their money step by step. In short, it’s a good balance between autonomy and security, which reassures parents while motivating teens.

Pixpay card

Revolut Kids & Teens: a junior version of the famous neobank

Revolut Kids & Teens is the junior version of the renowned international neobank Revolut. Available from 6 years old, it allows children and teens to use a real debit card linked to a parent’s Revolut account. The offer is free, making it an interesting solution for families already using the bank regularly. Young people can pay in-store, online, or withdraw small amounts, with limits appropriate to their age. Parents of course keep control via the app, and each expense is visible immediately, and it’s possible to adjust or block the card in seconds.

The clear and accessible interface helps children gradually learn money management. Revolut Kids & Teens stands out mainly for its simplicity and excellent value for money.

Revolut Kids & Teens card

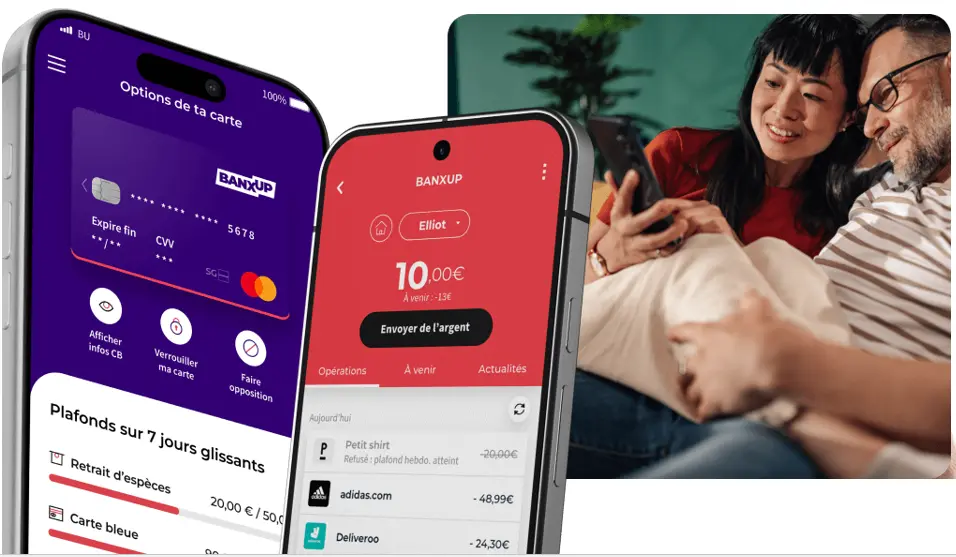

Banxup: a teen card to learn how to manage money, under parental supervision

The Banxup card offered via Société Générale is aimed at young teens who want to start managing their money on a daily basis, while staying accompanied. Specifically, this is an account linked to a bank card, all accessible from a mobile app. On the parents’ side, a dedicated space allows tracking expenses, adjusting spending limits, or authorizing (or not) certain types of payments.

The appeal of Banxup lies mainly in its progressive approach. The teen can pay, check their balance, track expenses to get used to the basics of budgeting. For parents, they keep an eye on card usage without falling into excessive control.

Less playful than some neobanks for youths, Banxup focuses more on a reassuring, educational framework. It’s an interesting solution for a first card, especially if the aim is to learn to manage money simply, step by step.

Banxup card

How to choose the right bank card for a minor?

Choosing the right bank card for a teenager is primarily about finding the one that fits their age and how they will use it. Needs obviously differ whether you’re 11, 14, or 17.

Around 10 or 11 years old, a bank card mainly serves to learn the basics: how to withdraw a little cash, pay small purchases (a few candies, a snack after school, a book, or a small treat), and understand that spending is limited to what is available on the account. In this phase, parents must maintain strict control, with the possibility to block the card or set very low limits.

From 13 or 14 years old, expectations change. The teenager starts going out more often, managing their own activities (their bus pass, a sandwich at the local snack bar) or their first school trips. They then appreciate a more flexible card, with an app that gives them a clear view of their expenses and helps them become more responsible.

Finally, as they approach 16 or 17 years old, the bank card becomes almost indispensable, particularly for managing money earned during summer jobs, online shopping, paying for gasoline and scooter insurance, or financing somewhat larger purchases. At this stage, the teen seeks more autonomy, but the educational role of the card remains essential. The right choice thus depends on finding the right balance between safety for parents and increasing freedom for the child.

What are the advantages and drawbacks of a bank card for a teenager?

While it is highly recommended to get a teenager used to using a bank card and taking responsibility for managing their money early, it’s important to remember that this type of tool is not without limits. As with most things, there are positive aspects but also constraints. Let’s explore the main advantages and disadvantages of a bank card for a teen.

What are the advantages of a card for teens?

- Gradual learning: the teen discovers the value of money and learns to manage a budget in real conditions.

- Enhanced security: there is no risk of overdraft, adjustable limits, and the possibility to block the card remotely.

- Autonomy valued: the child can pay daily purchases without handling large sums in cash.

- Modern educational tool: some cards come with fun apps that encourage financial responsibility.

What are the disadvantages of a card for teens?

- Sometimes high cost: prices range from €2.99 to €4.99 per month for some cards, which can weigh on the family budget, especially if there are several teens.

- Limited features: these cards remain basic and do not replace a full bank account.

- Smartphone dependency: the effectiveness of the tracking often relies on using a mobile app.

- Risk of overspending: having a card on hand can encourage some teens to spend more easily.

All our information is, by nature, generic. It does not take into account your personal situation and does not constitute any personalized recommendations for the execution of transactions, nor can it be equated with financial investment advisory services or any incentive to buy or sell financial instruments. The reader is solely responsible for the use of the information provided, and no recourse against Cafedelabourse.com’s publishing company can be sought. The publisher’s liability cannot be engaged in case of error, omission, or inappropriate investment.